Spectra Adaptive

Market-Neutral

Survivorship-Bias Free

Multi-Factor

Top 30 Market Cap

Tier 3

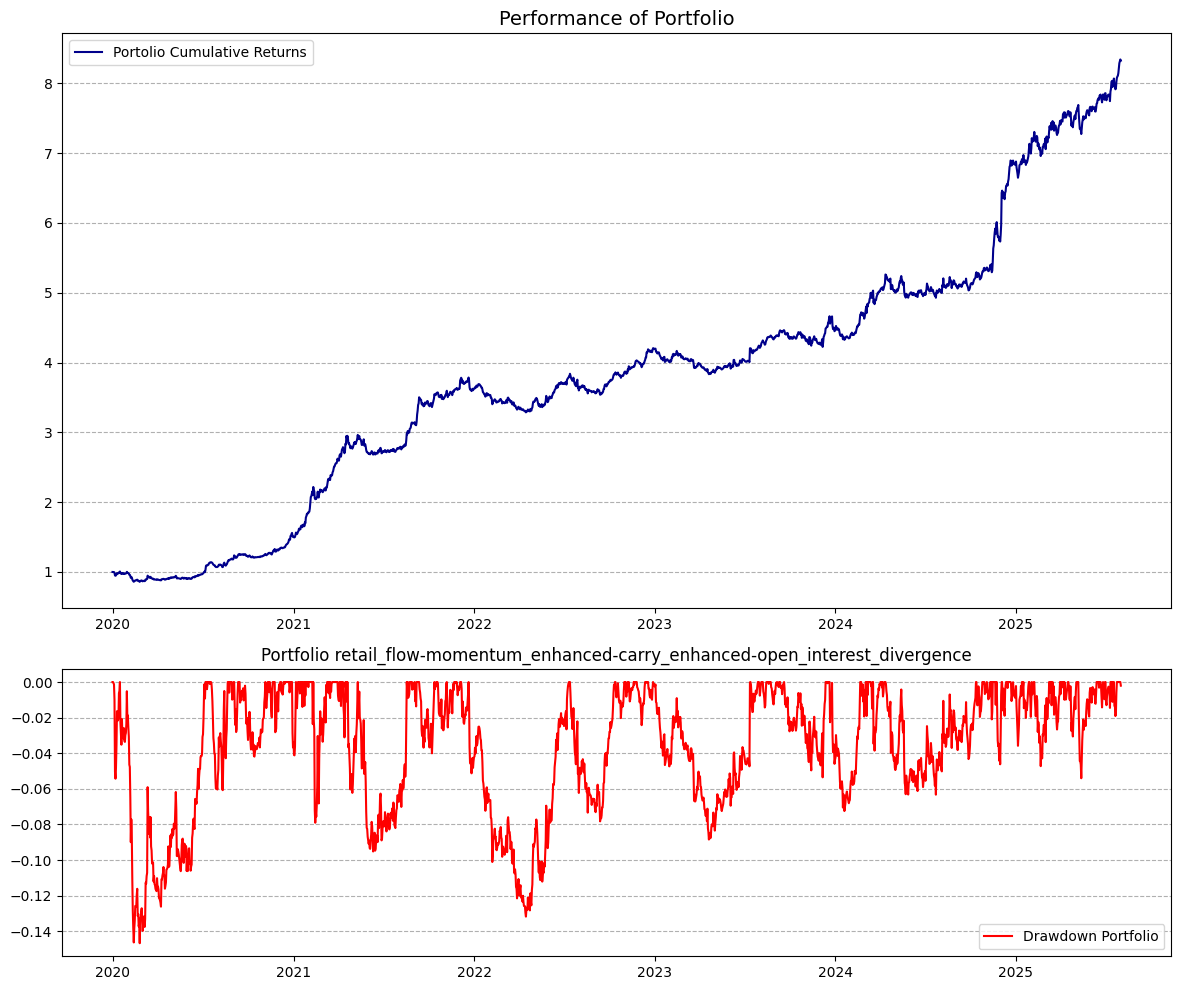

Spectra is a market-neutral portfolio that combines six orthogonal factors:

- Enhanced Momentum

- Enhanced Carry

- Retail Flow

- Margin Risk

- Altair

- Enhanced Mean Reversion

The Adaptive overlay reduces the portfolio's gross exposure when the market conditions are adverse. This may results in prolonged periods of very small (<10%) gross exposure.

The asset universe consists of the most liquid and actively traded assets, identified on rolling basis - various techniques employed to keep it both stable and relevant, as well as survivorship-bias free.

To balance each asset's risk contribution, positions are scaled according to the inverse of their rolling volatility.

The portfolio is rebalanced daily, at midnight UTC, weights are calculated at 23:55 and 00:15 UTC.

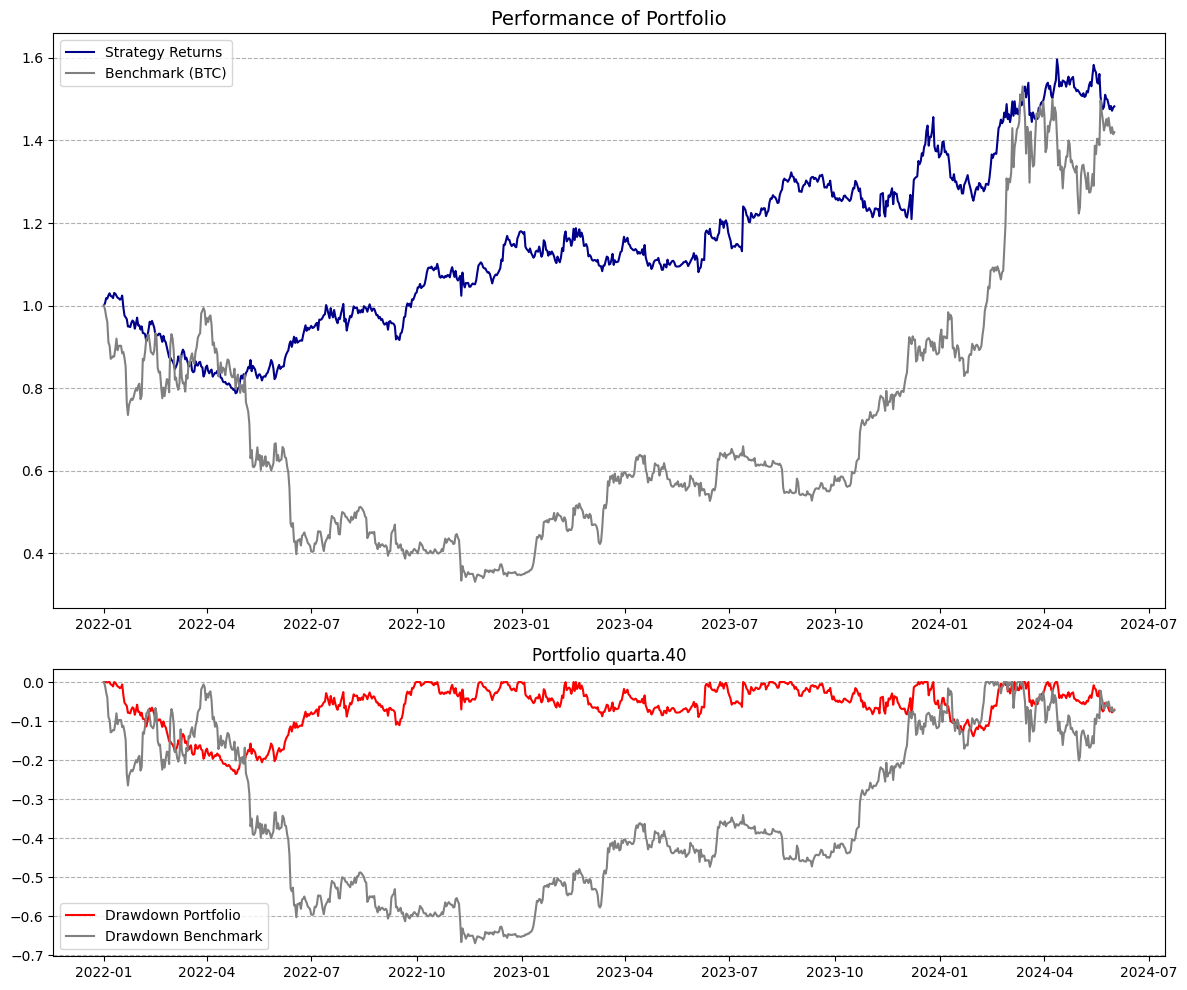

| Benchmark (BTC) | Portfolio | |

|---|---|---|

1.07 | 3.09 | |

59.5% | 124.6% | |

0.00 | 0.82 | |

1.00 | 0.04 | |

-76.6% | -17% | |

61.5% | 27.4% | |

0% | 46.2% | |

100% | 13.6% | |

100% | 123.6% |

Sharpe Ratio

Rolling 12 MonthsBeta

Rolling 12 Months - Benchmark: BTCNet Exposure of Portfolio

Portfolio Variants

Spectra Adaptive - Top 20 Market Cap

Tier 3

Combines 6 cross-sectional, orthogonal factors - while reducing exposure dynamically in adverse market conditions.

Spectra Adaptive - Top 40 Market Cap

Tier 3

Combines 6 cross-sectional, orthogonal factors - while reducing exposure dynamically in adverse market conditions.

Current Weights

10/22/2025, 12:09:53 AM (UTC)

Adaptive Portfolio weights can be all zero when the risk signal scales the portfolio weights down.

The portfolio is designed to be market-neutral on a volatilty-adjusted basis, therefore it may have net directional exposure on any given day. The weighting mechanism ensures that volatility-weighted directional exposure is negligible on the portfolio level.

| Ticker | Name | Arrival Price | Weight | Date |

|---|---|---|---|---|

| BTC | Bitcoin | 108380.006 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| ETH | Ethereum | 3874.6 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| SOL | Solana | 185.611 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| XRP | Ripple | 2.424 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| DOGE | Dogecoin | 0.194 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| SUI | Sui | 2.49 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| BNB | Binance Coin | 1057.127 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| ADA | Cardano | 0.643 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| LTC | Litecoin | 92.671 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| LINK | Chainlink | 17.626 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| ONDO | ONDO | 0.724 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| AVAX | Avalanche | 19.542 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| DOT | Polkadot | 3.006 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| BCH | Bitcoin Cash | 481.649 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| ENA | ENA | 0.454 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| PEPE | PEPE | 0.000006915438044725397 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| HBAR | Hedera | 0.171 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| TRX | TRON | 0.322 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| AAVE | Aave | 218.748 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| TAO | Bittensor | 381.853 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| NEAR | NEAR Protocol | 2.218 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| UNI | Uniswap | 6.253 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| APT | Aptos | 3.221 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| TON | Toncoin | 2.137 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| ETC | Ethereum Classic | 15.718 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| XLM | Stellar | 0.315 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| SHIB | SHIB | 0.000010057575520835404 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| HYPE | HYPE | 35.362 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| XMR | Monero | 304.964 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| WLFI | WLFI | 0.126 USD | 0.00% | 2025-10-22T00:09:53.394112+00:00 |

| 0.00% | ||||

Properties

Frequently Asked Questions

What is the construction methodology of the model portfolio on display? How do I replicate it?

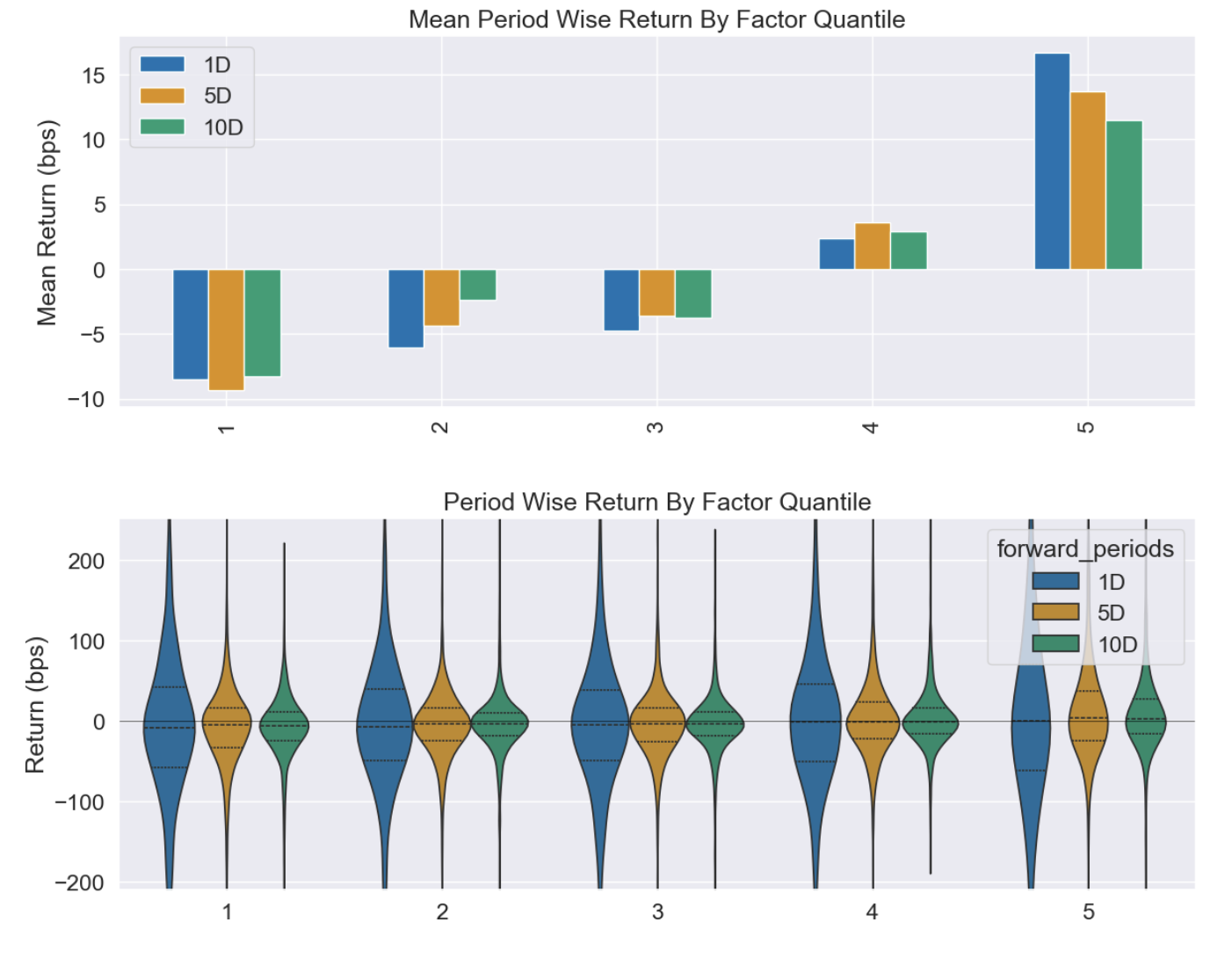

The portfolio is constructed by applying cross-sectional binning - quantiles. This ensures that the weights are calculated in proportion to the strength of the factor. The assets are then weighted according to the inverse of their rolling volatility, to mitigate the impact of widely different volatilities of digital assets. We provide a replication notebook in the "Resources" section that will produce a very similar portfolio than what's shown on the site.

Is the raw factor data available?

Yes, we serve the raw factor data via the "portfolio/factors" endpoint, please see the API Docs for more information.

What is smoothing? Some factors have by default setting (eg. 10 Day Moving Average) applied. Why is that?

Some of the cross-sectional factors have very high turnover, and despite being highly predictive, the alpha does not survive transaction costs. Smoothing (applying a simple moving average) is a way to reduce the turnover and the impact of transaction costs.

What is the universe of assets? How is it determined? Is it survivorship-bias free?

The universe of assets (there are multiple variants, for example, top 20, 30, 40 market cap digital assets) is the most liquid and actively traded assets, identified on rolling basis - various techniques (volume, open interest, volatility filters) are employed to keep it both stable and relevant. The universe is survivorship-bias free.

What is the rebalancing frequency?

The portfolio is rebalanced daily, at midnight UTC, weights are calculated at 23:55 and 00:15 UTC, and available point-in-time.

What are the transaction cost / slippage assumptions?

There are 0.05% transaction costs applied on each position adjustment. This is a parameter that can be adjusted in the backtest settings. Slippage, spread is not considered in the simplistic backtest that's on our site. We encourage using an independent backtesting infrastructure to validate performance.

When have been the factors developed? Is there an out-of-sample period?

Our cutoff date for our research process is 2024-01-01, we consider any data onwards as out-of-sample. Many factors have been traded live in some form from 2025-01-01.

Some of the factors look great! Should I pick an individual factor and start trading it?

We recommend using a portfolio of factors to maximize risk-adjusted returns. Alpha from individual factors is simply not consistent enough, and even running a simple arithmetic average of 3-5 relatively orthogonal factors will produce superior results.

Replication & API

Live Weights

Get live weights with the code provided below.