Cross-Sectional Alpha Factors for Crypto

Enhance risk-adjusted returns by overlaying crypto-native cross-sectional alpha factors on top of any HFT / MFT strategy. Bootstrap your crypto alpha research and go into production in days.

Factor BoardPoint-in-time

| Factor | |||

|---|---|---|---|

Supply Velocity On-Chain | +12.40% | +75.30% | |

Polaris Momentum | +24.46% | +53.20% | |

Altair Liquidity | +0.78% | +43.19% | |

Enhanced Carry Carry | +26.84% | +39.85% | |

Margin Risk Derivatives | +6.96% | +25.52% | |

Retail Flow Flow | +6.19% | -5.90% | |

Relative Illiquidity Liquidity | -4.82% | -13.73% |

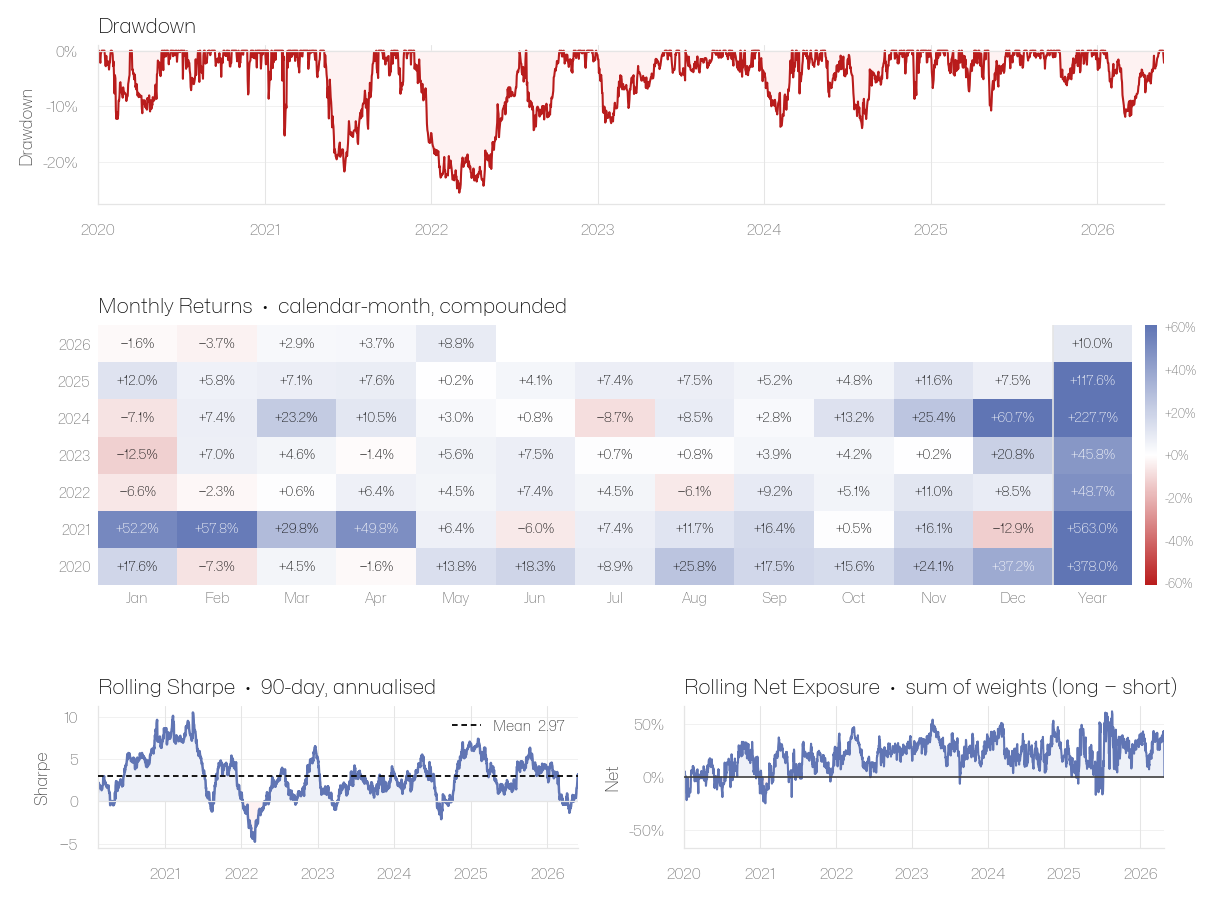

Top 40 Market Cap Universe - 200% Gross ExposureAs of Aug 10, 2026

Factor performance

Featured

Supply Velocity

supply_velocity.40

CAGR

+73.63%

Ann. vol (1Y)

27.4%

Sharpe (1Y)

2.16

Max drawdown

-42.4%

Top 40 Market Cap Universe - 200% Gross Exposure

Portfolio Highlight

Endorsed by

Trusted by further institutional partners under confidentiality

Accelerate Research to Deployment

Market-Neutral, Multi-Factor Portfolios

Institutional-grade, high-performance Factor Portfolios

Traditional and Proprietary Factors

Extensive collection of cross-sectional exogenous alpha & factor risk overlays.

Unique Datasets & Alpha Sources

Liquidity, Orderbook-derived, Flow, On-Chain & Sentiment factors.

Access Historical Data or Trial Live Data

Explore Notebooks

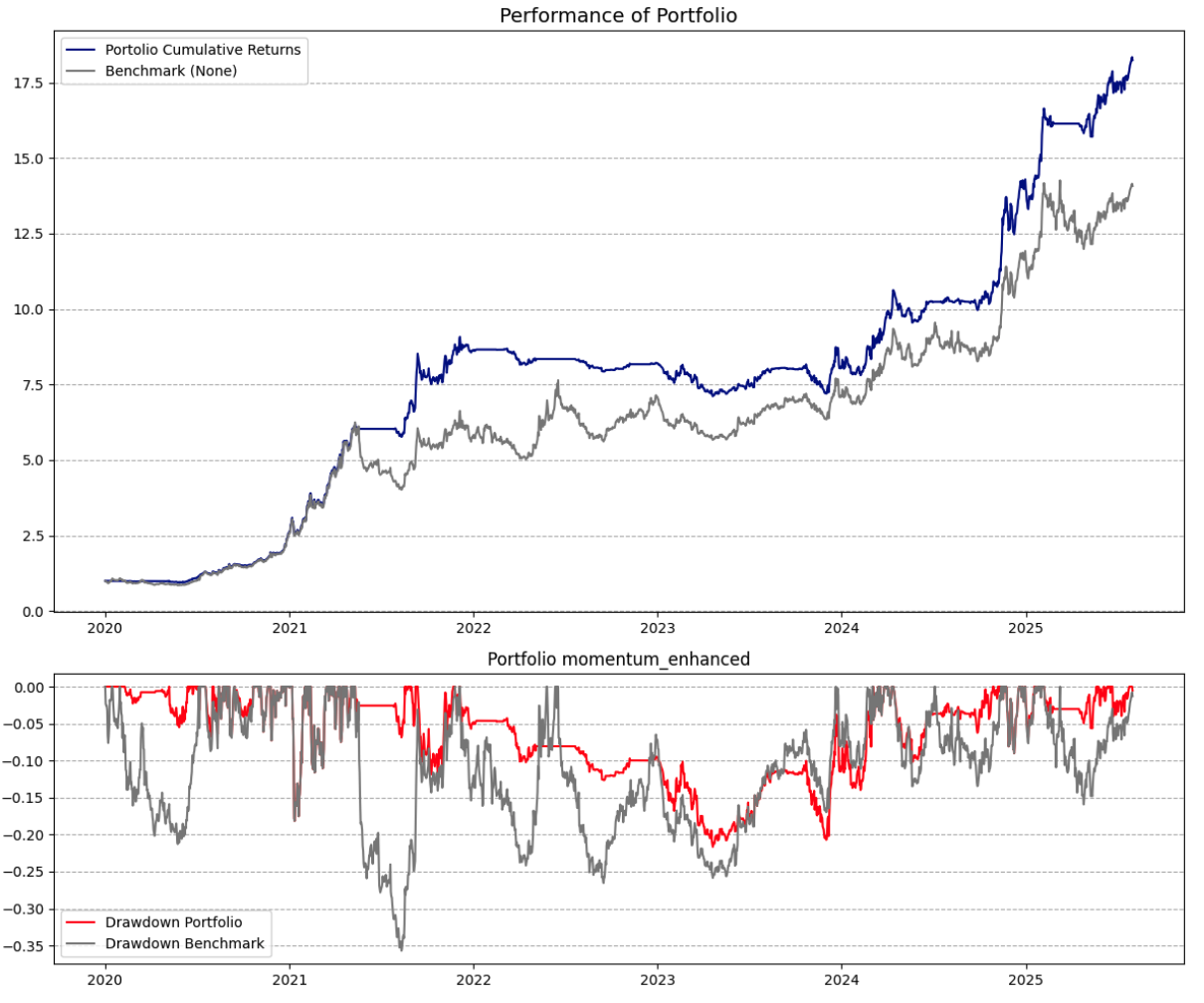

Replicate Spectra — our flagship multi-factor portfolio

Reproduce Spectra, our 6-factor market-neutral portfolio, from its constituent Unravel factors

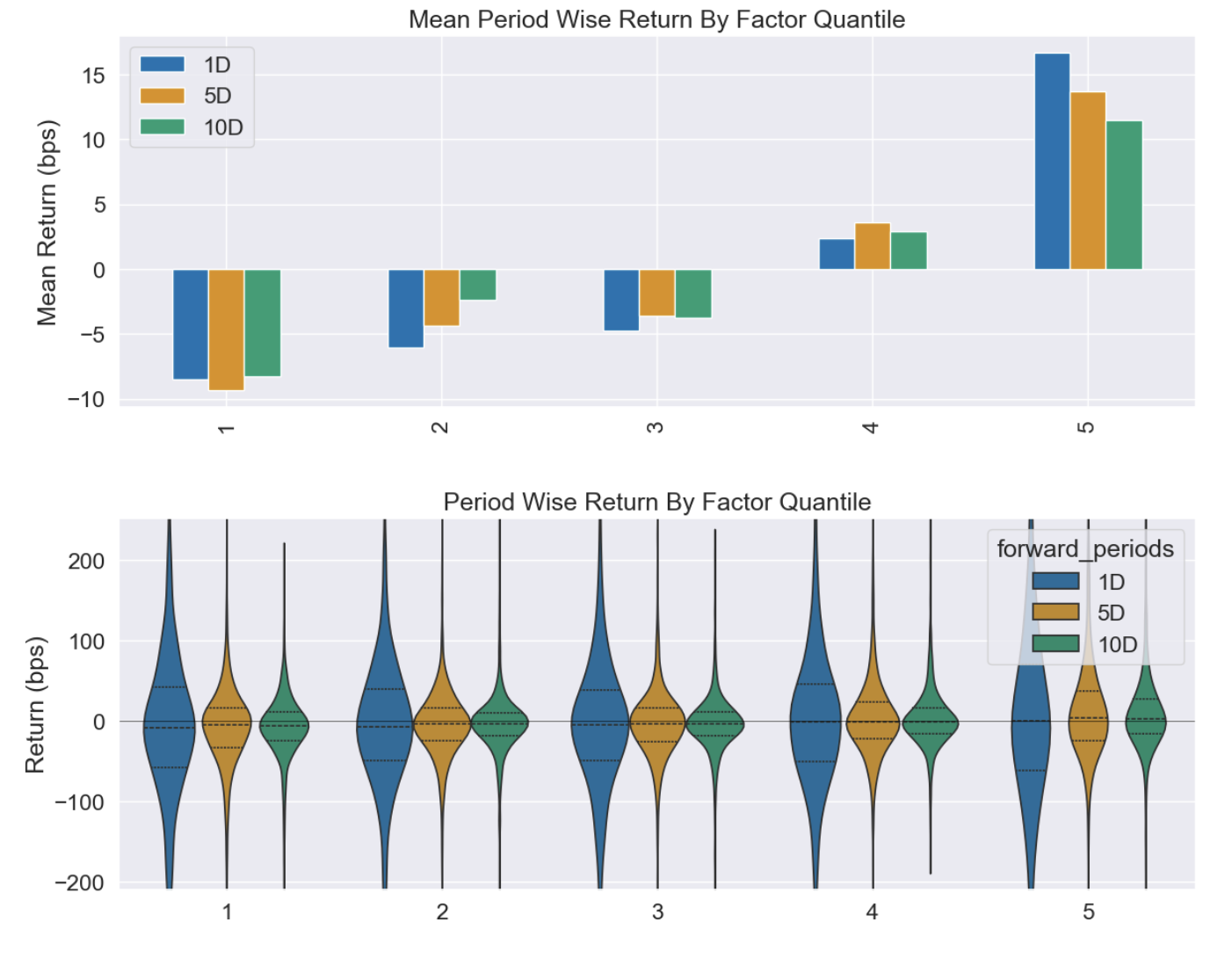

Retail Flow Factor Analysis

Retail Flow factor analysis with AlphaLens

Adaptive Portfolios with Risk Overlay

Replicate Adaptive portfolios with Risk Overlay using Unravel API

Get Started

Ready to deploy cross-sectional portfolios?

Schedule a consultation with our team to discuss your specific needs and how our institutional API can give you an edge.